It’s not news to say Great Britain’s electricity system is changing. Low carbon electricity sources are on course to go from 22% of national generation in 2010 to 58% by 2020 as installation of wind and solar systems continue to grow.

But while there has been much change in the sources fuelling electricity generation, the system itself is still adapting to this transformation.

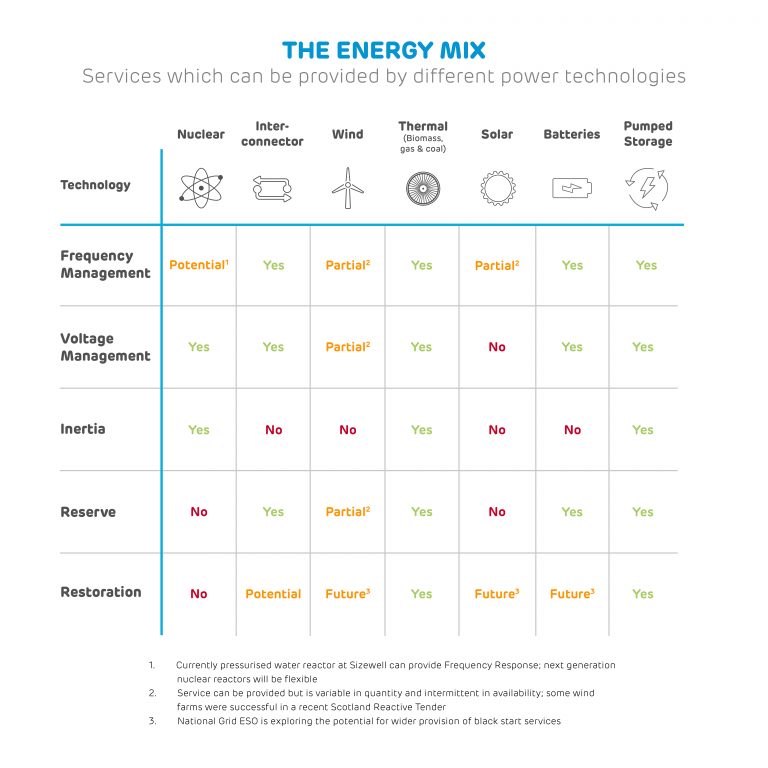

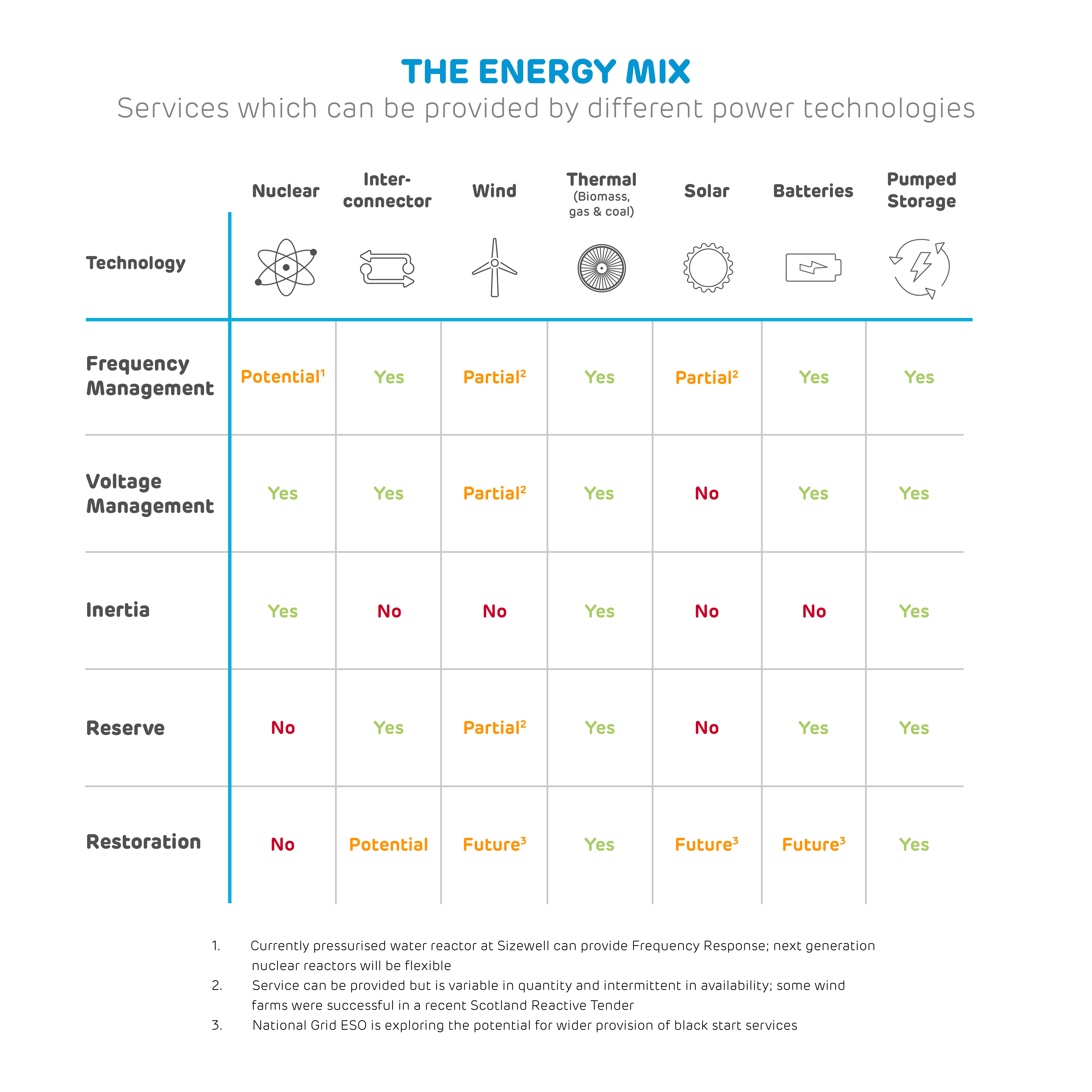

When the national grid was first established in the 1920s, it was designed with coal and big spinning turbines in mind. It meant that just about every megawatt coming onto the system was generated by thermal power plants. As a result, the mechanisms keeping the entire system stable – from the way frequency and voltage is managed to how to start up the country after a mass black out – relied on the same technology. These ‘ancillary services’ – those that stabilise the system – are crucial to maintaining a balanced electricity system.

“Ancillary services are needed to make sure demand is met by generation, and that generation gets from one place to the next with no interruptions,” explains Ian Foy, Head of Ancillary Services at Drax. “Because what’s important is that all demand must be met instantaneously.”

In today’s power system, however, weather dependent technology like offshore wind and home solar panels are increasingly making up the country’s electricity generation. Their intermittency or variability is, in turn, impacting both the stability of the grid and how ancillary services are provided.

Running a large power system with as much as 85% intermittent generation – for example on a very windy, clear, sunny day – is thought to be achievable. It isn’t a scenario anticipated for the large island of Great Britain. But to deal with the fast-pace of change on its power system which recently managed to briefly achieve 47% wind in its fuel mix, there is a need to develop new techniques, technologies and ways of working to change how the country’s grid is balanced.

New storage tech takes on balancing services

One of the technologies that’s expected to provide an increasing amount of balancing services is grid-scale batteries. One stabilisation function offered by batteries (and other electricity storage options) is to provide reserve at times when demand peaks or troughs. This matches electricity demand and generation.

Combined with their ability to respond quickly to changes in frequency, batteries can be a significant source of frequency response.

Batteries can also absorb and generate reactive power, which can then be deployed to push voltage up or down when it starts to creep too far from the 400kV or 275kV target (depending on the powerlines the electricity is travelling along) needed to safely move electricity around the grid.

The challenge with batteries is that the quantity of megawatt hours (MWh) required to compensate for intermittency is very large. The difference between the peak and trough on any day may be more than 20 GW for several hours (see for yourself at Electric Insights).

The significant price reductions in battery storage apply to technologies with short duration (or low volume MWhs). These are the technologies which have been developed at scale recently but will probably struggle to make up in any large quantity any shortfalls in generation resulting from prolonged periods of low intermittent generation.

A challenge currently being addressed relates to maintenance of battery state of charge. This is a consequence of battery storage having a cycle efficiency of less than 100%. This means that losses from continuous charging and recharging will have to be replenished from the available generation to avoid batteries going empty and being unavailable for grid services.

Ultra-low carbon advances

Rather than relying on batteries to provide ancillary services to support intermittent generation, technical advancements are allowing the wind and solar facilities – which are generating more and more of the country’s electricity – to do so themselves.

The traditional photovoltaic (PV) inverters found on solar arrays were initially designed to push out as much active, or real, power as possible. However, new smart PV inverters are capable of providing or absorbing reactive power when it is needed to help control voltage, as well as continuing to provide active power.

The major advantage of smart inverters is the limited equipment update required to existing solar farms to allow them to offer reactive power control. The challenge here is that PV is embedded in distribution systems and therefore reactive services they provide may not cure all the problems on the transmission system.

Similarly, existing wind installations have traditionally focused on getting the greatest amount of megawatts from the available resources, but with fewer thermal power stations on the grid, ways of balancing the system with wind turbines are also being developed.

Inertia is the force that comes from heavy spinning generators and acts as a damper on the system to limit the rate of change of frequency fluctuations. While wind turbines have massive rotating equipment, they are not connected to the grid in a way that they automatically provide inertia, however, research is exploring what’s known as ‘inertial response emulation’ that may allow wind turbines to offer faster frequency response.

This works through an algorithm that measures grid frequency and controls the power output of a wind turbine or whole farm to compensate for frequency deviations or quickly provide increases or decreases in power on the system. Inertial response emulation cannot be a complete substitute for inertia but can reduce the minimum required inertia on the system.

Even in a future where the majority of the country’s electricity comes from renewable sources, thermal generators may still be able to provide benefits to the system by running in ‘synchronous compensation’ mode i.e. producing or consuming reactive power without real power.

However, what is vitally important for the future of balancing services in Great Britain is a healthy, transparent and investable market for generators, demand side response and storage, whether connected on the transmission or distribution networks.

A market for the future grid

One of the primary needs of balancing service providers is greater transparency into how National Grid procures and pays for services. Currently, National Grid does not pay for inertia. With it becoming more important to grid stability, incentive is needed to encourage generators with the capability to provide it. Those technologies that can’t provide inertia, could be encouraged to research and develop ways they could do so in the future.

Standardising the services needed will help ensure providers deliver balancing products to the same level needed to support the grid. It would also benefit from fixed requirements and timings for such services. Bundling related products, such as reserve and frequency control, and active power and voltage management, will also offer operational and cost efficiencies to the providers.

Driving investment in balancing services for the future, ultimately, requires the availability of longer-term contracts to offer financial certainty for the providers and their investors.

Bridge to the future

Click to view larger graphic.

For the challenges of decarbonisation to be met in a socially responsible way, Great Britain’s power system must be operated at as low a cost as possible to consumers.

With new technologies, almost anything could be possible. But operating them has to be affordable. In many cases, it may take time for costs of long duration batteries to come down – as it has with the most recent offshore wind projects to take Contracts for Difference (CfDs) and Drax’s Unit 4 coal-to-biomass conversion under the Renewables Obligation (RO) scheme.

Thermal power technologies such as gas that has proven capabilities in ancillary services markets can at least be used in a transitional period over the coming decades until a low carbon solution is developed.

Biomass will continue to be an important source of flexible power. This summer, at Drax, biomass units are helping to balance the system. It is the only low carbon option which can displace the services provided by coal or gas entirely.

Drax Power Station’s control room. Viewing on a computer? Click above and drag. On a phone or tablet – just move your device.

In the past the race to decarbonisation was largely based around building as great a renewable capacity as possible. This approach has succeeded in significantly scaling up carbon-free electricity’s role on Great Britain’s electricity network. However, for the grid to remain stable in the wake of this influx, all parties must adapt to provide the balancing services needed.

This story is part of a series on the lesser-known electricity markets within the areas of balancing services, system support services and ancillary services. Read more about black start, system inertia, frequency response, reactive power and reserve power. View a summary at The great balancing act: what it takes to keep the power grid stable and find out what lies ahead by reading Maintaining electricity grid stability during rapid decarbonisation.

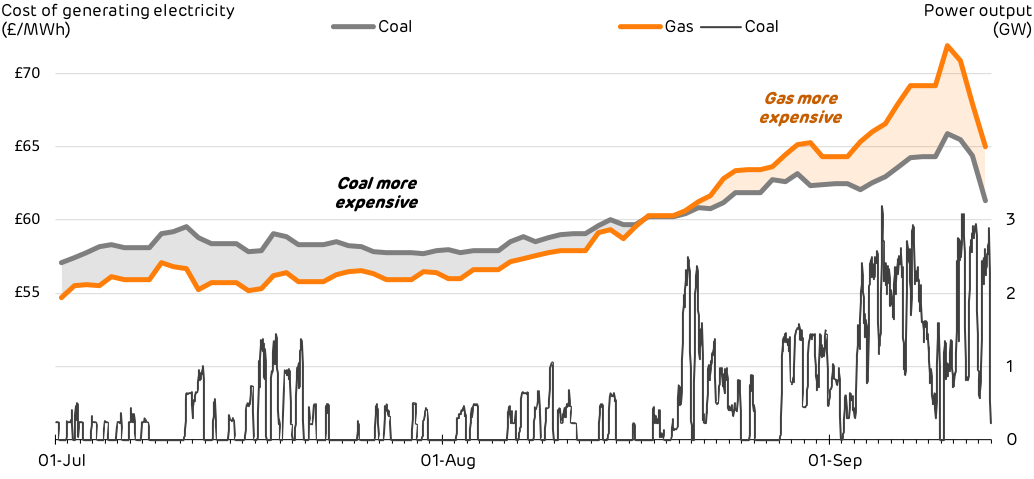

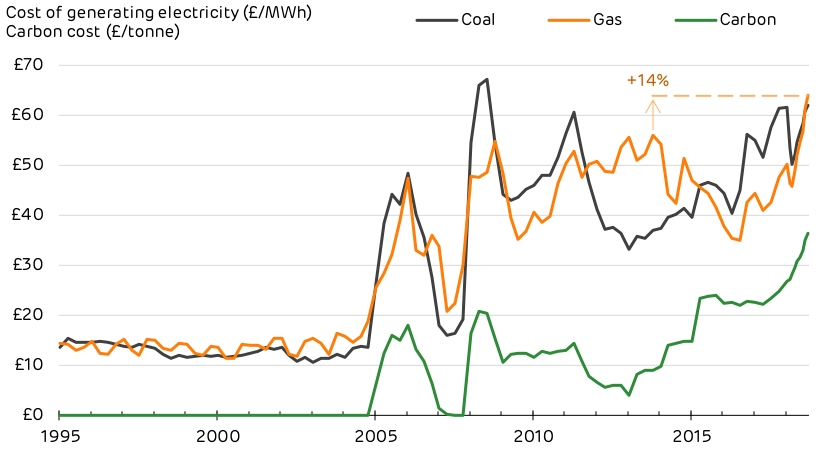

This Carbon Price Support has had a huge impact, particularly on coal. Prior to its introduction, coal represented 50% of power generation but since it has fallen to record lows. 2017 saw the first day without any coal on the power system since the industrial revolution. Records continue to be broken throughout 2018, with

This Carbon Price Support has had a huge impact, particularly on coal. Prior to its introduction, coal represented 50% of power generation but since it has fallen to record lows. 2017 saw the first day without any coal on the power system since the industrial revolution. Records continue to be broken throughout 2018, with

Thursday 1 March was the coldest spring day on record, averaging –3.8°C. The six days from 26 February to 3 March (highlighted in blue) were the coldest Britain has been since Christmas 2010.

Thursday 1 March was the coldest spring day on record, averaging –3.8°C. The six days from 26 February to 3 March (highlighted in blue) were the coldest Britain has been since Christmas 2010.