- Reaching net zero while delivering economic growth requires both energy security and carbon removals.

- In the late 2020s, UK demand for energy is set to exceed secure and dispatchable supply by 5GW at peak times – leaving the country dependent on imported and intermittent sources to avoid shortages.

- To bridge the energy security gap the Government needs to extend the lives of existing assets, including biomass and nuclear plants, and curb peak demand.

- Drax plans to install Bioenergy with Carbon Capture and Storage (BECCS) at Drax Power Station, if we secure the right support from Government this project will ensure the site continues to keep the lights on for millions of homes and businesses well into the future.

- BECCS is a unique technology, nothing else generates renewable power while removing carbon from the atmosphere.

- Bridging support for Drax Power Station from 2027 as a pathway to BECCS will mitigate the energy crunch and reduce dependency on intermittent generation.

- There is a huge opportunity for carbon removals technology to assist with other industries in decarbonising, and further opportunities to reduce cost by sharing resources.

- BECCS is only possible if we ensure high standards for carbon removals, and these standards must acknowledge the difference between engineered and natural solutions.

We all know that action is needed to tackle the global climate emergency. If we get these changes right, they will ultimately be beneficial to economies and society.

Industries of all kinds will need to reduce their CO2 emissions. While reducing greenhouse gas (GHG) emissions is vital, it is becoming clear that reductions alone are unlikely to be enough: it will also be necessary to remove GHGs from the atmosphere to limit the global temperature increase to 1.5C. Any residual emissions in hard-to-abate sectors like aviation or agriculture will require carbon removals at scale, in both a combination of nature and technology-based carbon removal solutions.

This vision of the future doesn’t have to mean low-growth economies or scarce energy supply. Instead, we can build and adapt our energy systems for a sustainable future that enables prosperous economies and thriving societies.

Today, energy systems are some of the world’s most emission-intensive sectors, though many are rapidly decarbonising. The UK has made excellent progress in delivering this, ahead of many other countries, with around 60% of its power now coming from low-carbon sources.

The continued evolution of the energy industry is also intrinsically connected to delivering carbon removals at scale.

The two primary engineered carbon removals technologies are BECCS and Direct Air Capture and Storage (DACS). DACS can remove CO2 from ambient air and then store it underground. To do so, DACS requires a low carbon source of power. BECCS, by contrast, generates power using renewable biomass that absorbs CO2 as it grows. The CO2 is then captured and stored safely and permanently underground.

Done right, they both remove more CO2 than they emit – delivering carbon removals. But BECCS’ unique capability to deliver carbon removals while generating 24/7 baseload power means it can support energy security while helping to tackle climate change.

Delivering energy security in a net zero future

As society electrifies to meet net zero, the demand for power will substantially increase. Meeting these increases will require governments to work with the private sector to deploy a range of technologies. Increasing deployment of renewables like wind and solar around the world will be vital. But these intermittent sources will need complementary technologies like short and long-term energy storage, as well as baseload power generation that can ensure energy systems remain secure and stable.

BECCS is the only renewable energy and carbon removal technology that offers the full suite of system support services. This includes a reliable, stable source of power integrated with other intermittent renewables, something that will only become more important as energy systems decarbonise.

One example of the role biomass can play in global energy solutions comes from research we commissioned from Baringa, which finds that peak demand for UK energy will increase by up to 7GW by 2027. The closure of coal, older gas, and nuclear power stations, however, will also remove up to 7GW of secure capacity from the grid. This could be further exacerbated by ongoing costly delays in new power plants such as Hinkley Point C, which is not expected to be completed until 2031. This means the percentage of ‘secure’ capacity needed to cover peak demand in the UK is projected to decrease

Recent independent analysis by Public First, reaffirms that the UK will hit an energy security “crunch point” in 2028, and the UK’s demand for power is set to exceed secure dispatchable and baseload capacity by 7.5GW. This shortfall would leave the UK more dependent on intermittent domestic and international generation.

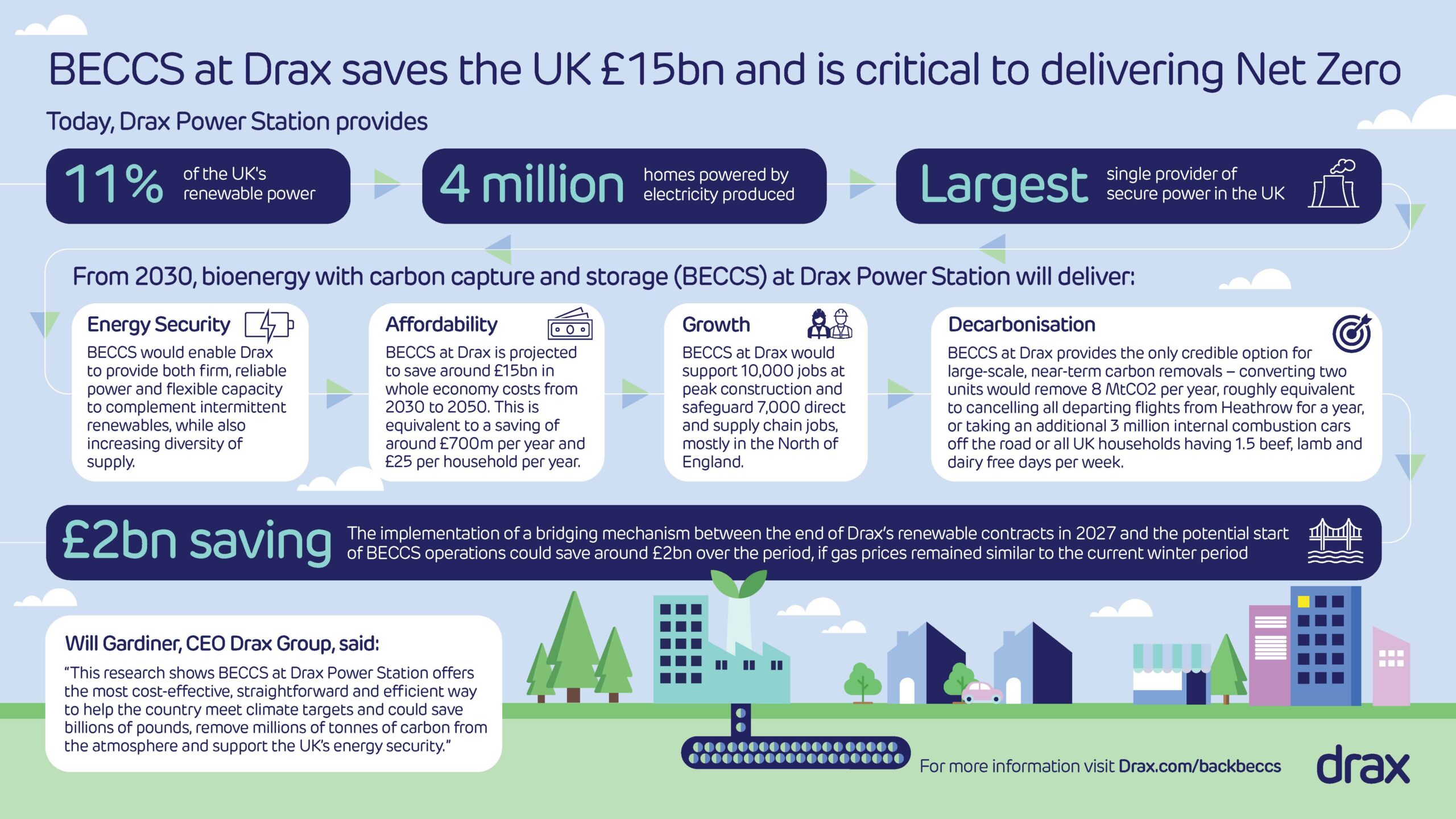

Therefore, existing assets like Drax Power Station will be even more critical to energy security. Bridging support for Drax Power Station from 2027 until BECCS is online will reduce the risk of energy shortages and reduce dependency on overseas sources, supporting energy security and decarbonisation through the crunch.

The Government’s Powering Up Britain strategy aims to set the course for delivering the UK’s net zero and energy security ambitions. A key part of this programme is carbon removals and the development and deployment of large-scale Power BECCS by 2030.

We’ve shown at our North Yorkshire site how BECCS is ready to work within the current energy ecosystem. It’s an opportunity to utilise existing infrastructure, convert coal power stations and adapt to an energy secure, net zero future.

In January 2024, the Secretary of State for Energy Security and Net Zero, Claire Coutinho, approved the Development Consent Order (DCO) for our plans to convert two biomass units at Drax Power Station to BECCS.

Providing the coming months see real progress in our discussions and there is swift decision making, we stand ready to invest billions to develop what will become world’s largest engineered carbon removals project at Drax Power Station.

Our plans for Power BECCS in North Yorkshire would enable us to remove up to eight million tonnes of CO2 from the atmosphere per year, while still generating secure, dispatchable, renewable power for millions of homes and businesses.

Without BECCS at Drax, the UK’s target of five million tonnes of carbon removals by 2030 would be difficult to achieve. The pioneering project would build on Yorkshire’s proud industrial heritage, as well as potentially delivering more than 10,000 jobs at the height of construction and position the county and the UK as leaders in the race to create and scale a technology required to capture greenhouse gas emissions.

The DCO approval is another milestone in the development of our BECCS plans and demonstrates both the continued role that Drax Power Station has in delivering UK energy security and the critical role it could have in delivering large-scale carbon dioxide removals to meet net zero targets.

It offers a model for energy security globally. While ensuring the phase-out of fossil fuels around the world, biomass offers a renewable, flexible alternative to reduce our dependency on forms of power such as coal. With BECCS, we can go further by transforming existing coal power stations from carbon emitters into carbon removers.

Decarbonisation across industries

Carbon dioxide removal technologies, like BECCS and DACS, can neutralise hard-to-abate and residual emissions across whole industrial clusters.

Furthermore, carbon removal hubs or clusters, with shared decarbonisation goals, technology, and infrastructure, offer locations where BECCS and DACS can help emissions-intensive industries decarbonise. Sharing infrastructure, like pipelines and storage locations can reduce the cost of deploying carbon removals by creating economies of scale.

Major industries like steel, cement, and chemicals, that employ millions of people around the world may only be viable in a net zero future with connections to carbon removals technologies. BECCS also offers these industries, that depend on energy-intensive processes, an alternative source of power from fossil fuels.

Baringa’s analysis found that Drax’s proposals for BECCS at Drax Power Station could save the UK up to £15bn in whole economy costs in meeting the country’s net zero goals between 2030 and 2050. It also demonstrates that without BECCS at Drax, meeting carbon reduction targets is more complicated and expensive and carbon savings would be needed in other sectors.

Research by the Intergovernmental Panel on Climate Change, the world’s leading authority on climate science, also states that to tackle climate change, up to 9.5 billion tonnes of carbon removals via BECCS will be required globally per year by 2050. So as the world enters the pivotal decades to act on the climate crisis, governments around the world must take action. One idea of a decarbonisation hub is included in the U.S. Inflation Reduction Act, which commits $3.5 billion to developing four regional Direct Air Capture Hubs.

The Inflation Reduction Act’s total $369 billion funding package focused on energy security and climate change contains a host of potential opportunities for BECCS deployment across renewable power generation, sustainable aviation fuel and hydrogen.

These include a $40 billion loan fund for projects which utilise innovative technology to reduce, avoid or sequester carbon, and $140 million to create a competitive purchasing programme for carbon removals.

Furthermore, the act increases the availability of the 45Q tax credit for carbon capture and storage projects, increasing their value from $50 a tonne of carbon removals to $85 per tonne. These are all promising steps to creating the market and environment needed to deploy technologies like BECCS and DACS.

We recently announced that we’re launching a new business focused on becoming the global leader in large-scale carbon removals, which will oversee the development and construction of our new-build BECCS plants in the US. These projects, through the investment they attract and the jobs they generate, can become key economic drivers in a given region.

The global opportunity for BECCS is clear. The market for carbon removals is growing. And we want to ensure BECCS offers a high-integrity form of carbon removals that delivers permanent carbon sequestration.

Ensuring high quality carbon markets

As pioneers in the field, we’re setting the bar for carbon removal standards, ensuring quality is intrinsic to Drax’s offering. To help achieve this, we’ve partnered with Stockholm Exergi and EcoEngineers to develop a world-leading methodology to ensure the integrity of BECCS carbon removals. Our paper, ‘Corporate climate claims: The case for including permanent carbon removals’ also looks at resetting the standard on corporate claims for carbon removals. Tackling climate change while advancing sustainability is at the heart of our purpose and we’re committed to supporting organisations – especially those with hard-to-abate emissions – work towards decarbonising and reaching climate targets.

From the biomass used to fuel BECCS, to capture and transport processes, it’s imperative the carbon removed is always greater than any carbon emitted throughout the process.

Building from a sustainable base, with a high set of standards can make BECCS a transformational technology in powering the future and delivering carbon removals. No other technology can do both. BECCS can generate renewable power. BECCS can remove emissions. BECCS can deliver a prosperous, net zero future for the world.

To find out more about BECCS and how carbon removals can support your company’s decarbonisation journey, visit draxcarbonremovals.com